Fintech buyers in 2026 are asking AI. A $5M ARR B2B fintech founder shortlisting business banking like Mercury, Rho, and Ramp. An insurtech head of finance comparing Brex versus Rho for a 40-person company. A CFO at a Series B SaaS evaluating Modern Treasury and Column for embedded payment rails. A startup CFO picking between Carta, Pulley, and AngelList Stack for cap table management. A crypto startup operator comparing Increase and Treasury Prime for FBO accounts. Five years ago those questions started on Google with “best business bank account” or “Stripe vs Adyen.” Today, increasingly, they start with a prompt in ChatGPT, Perplexity, or Claude, and the answer comes back as a ranked table of three to ten vendors with stage-aware reasoning and integration verdicts.

We ran the experiment ourselves. We asked ChatGPT the most common commercial fintech infrastructure query a buyer might type, framed by stage. Here is what came back.

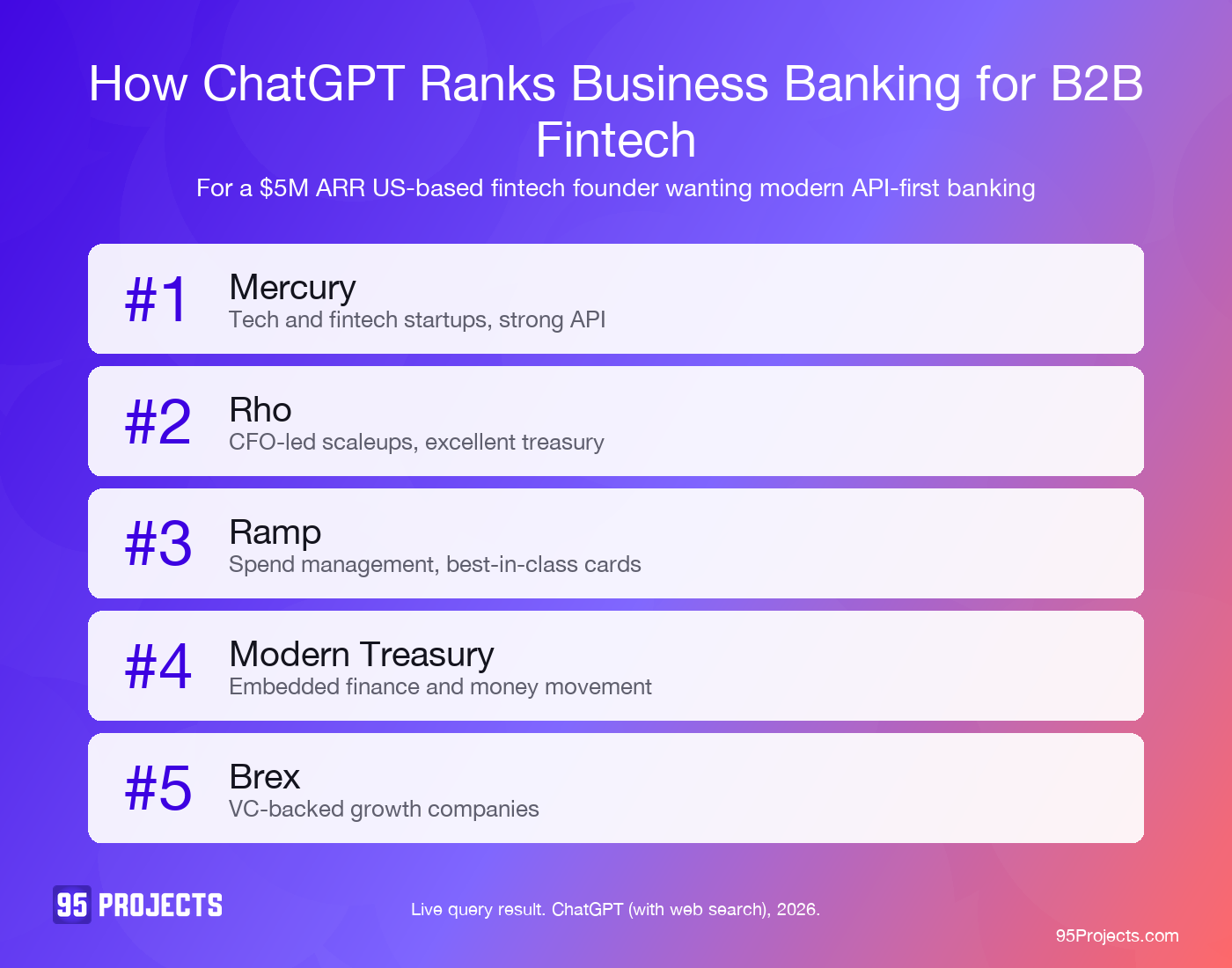

For “best business banking and corporate card platforms for a $5M ARR B2B fintech startup in 2026” (with the buyer framed as a US-based founder/CFO wanting modern API-first banking, skipping JPMorgan and Chase), ChatGPT returned a ranked table of seven vendors led by Mercury, then Rho, Ramp, Modern Treasury, and Brex, with Column, Treasury Prime, and Increase named as infrastructure-layer options for embedded use cases. The most interesting result was that the response immediately ruled out the legacy banks the buyer mentioned and surfaced an entire stack of fintech-native challengers, with their relative strengths broken out by API quality, treasury sophistication, and stage fit.

ChatGPT ranking of business banking for a $5M ARR B2B fintech, captured 2026

The pattern is clear and it cuts against the assumption most fintech marketing teams operate on. ChatGPT does not just default to the biggest brand in the category. When the buyer signals stage (ARR, team size, stack) and motion (API-first, embedded, treasury-heavy), it actively ranks stage-appropriate fintech challengers above incumbents. If your fintech is in the right niche for the right buyer and is not in those tables, you are invisible to a meaningful and growing slice of your category demand. This guide is the open-book playbook for getting in.

Fintech buyers, whether they are a founder picking the company’s first bank account, a CFO at a Series B scaleup choosing AP automation, a head of treasury sizing payment rails, a head of compliance shortlisting KYC/AML platforms, or a head of risk picking fraud tools, do not search like Google users. They prompt like operators. They ask comparative, stage-aware, integration-conscious questions and expect ranked answers with reasoning about API quality and regulatory fit.

Here is the pattern across the commercial fintech queries we tested:

Stage-tag your positioning (“for $1M to $50M ARR fintechs”) on every page

“Best [category] for [use case] (embedded, treasury, B2B payments)”

Use-case-filtered shortlist with API verdict

Use-case landing pages outperform generic category pages every time

“[Tool A] vs [Tool B] for [stack / region]”

Comparison matrix with API quality, banking, cards, treasury columns

Honest, detailed comparison pages with integration notes get cited verbatim

“Best alternatives to [incumbent: Stripe / Plaid / SVB]”

Challenger list with positioning blurbs (Mercury post-SVB era)

Position explicitly as the alternative on your pages and in vendor comparison content

“Cheapest [category] with [feature set]”

Price-tier filtered shortlist with feature crossover notes

Transparent pricing pages with itemized feature breakdowns get cited disproportionately

The fintech buyer landscape spans more roles than just the founder or CFO. Here are the segments that actually drive fintech software shortlists today, with the kinds of prompts each role types:

Buyer Segment

Sample AI Prompts

Founder / CFO (seed to $5M ARR fintech)

“Best business banking for an API-first B2B fintech”, “Mercury vs Brex for a 10-person startup”

Head of Finance / Controller (Series A to C)

“Best AP automation for a $10M ARR B2B SaaS”, “Rho vs Ramp for spend management”

Head of Treasury

“Best treasury management for a $50M ARR fintech”, “Modern Treasury vs Increase for money movement”

Head of Compliance / BSA officer

“Best KYC and AML platforms for B2B fintech”, “Persona vs Alloy vs Sardine for fraud”

Head of Risk / Underwriting (lending fintech)

“Best risk decisioning platforms for a small business lender”, “Taktile vs Provenir”

Head of Engineering / CTO (embedded fintech)

“Best ledger APIs for embedded payments”, “Modern Treasury vs Increase vs Column for FBO accounts”

Head of Card / BIN sponsor (card fintech)

“Best card issuing platforms for a B2B fintech”, “Marqeta vs Highnote vs Lithic”

Operations lead (mid-market fintech)

“Best reconciliation and bookkeeping tools for fintech”, “Puzzle vs Pilot vs Mosaic”

How AI search engines decide what to recommend in fintech

Across the queries we ran, ChatGPT cited five categories of source. The fintech surface area is distinct from other B2B verticals: it leans heavily on practitioner-led financial media, Reddit discussions, and the publications operators actually read in finance leadership roles. We expected to see Gartner and Forrester dominate. The reality was different:

Source Category

Examples ChatGPT Actually Cited

Why It Works

Tier-2 financial and fintech media

Wall Street Journal, Fintech Business Weekly, The Information, Finimize, Bank Director

Practitioner-edited financial publications carry trust signals AI engines weigh heavily for fintech buyer queries

Niche fintech category review and comparison sites

waveup, Founder Pass, Operator-focused review blogs (the ones operators actually read at $1M to $50M ARR)

Single-category specialist content focused on fintech infrastructure cites and gets cited disproportionately

Real founder and operator threads with “we switched from X to Y” stories

ChatGPT explicitly quotes Reddit threads where operators describe real bank, card, and treasury switching experiences

Vendor-owned comparison and alternative pages

Vendor “vs” pages, “alternatives to Mercury” pages, “Stripe alternatives” pages

Honest “where we lose” comparison pages from challenger fintechs get cited directly. The skeptical fintech buyer values fairness

Founder and operator newsletters and podcasts

First Round Review, a16z fintech content, Not Boring (Packy McCormick), Fintech Brainfood, Lenny’s Newsletter

Operator-led editorial outperforms enterprise analyst content for fintech category queries because the audience writes the audience’s prompts

Notice what is NOT on that list as the primary surface: Gartner, Forrester, IDC. They are in the underlying data, but they are not what ChatGPT cited inline for stage-aware mid-market fintech prompts. That is not what most fintech marketing teams expected before running the experiment.

Each surface has its own access and trust signals. Here is what actually drives whether ChatGPT cites your fintech inside them:

Citation Driver

Why It Matters for Fintech

Mentions in tier-2 financial publications (Wall Street Journal, Fintech Business Weekly, etc)

A single fintech-press mention carries more AI search weight than dozens of generic SaaS review-site profiles for category queries

Honest vendor comparison and “vs” pages

ChatGPT lifts comparison verdicts verbatim from vendor pages that read as fair. Fintech buyers are skeptical, so honest comparisons outperform marketing fluff at orders of magnitude

Reddit and operator community presence

Founder threads in r/Entrepreneur and r/fintech where someone describes real switching experience feed ChatGPT directly. Operator-tone wins, marketing-tone gets filtered

Stage-tagged and use-case-tagged positioning on your own pages

Pages that explicitly say “for $1M to $20M ARR fintechs” or “for B2B SaaS embedded payments” get pulled into stage-aware and use-case-aware queries

Operator newsletter and podcast features

Being featured in Fintech Brainfood, Not Boring, or a Packy McCormick deep dive carries practitioner credibility that ChatGPT weighs heavily for category context

Curious where your fintech shows up in ChatGPT?

We run free AI search audits across the prompts that match your fintech category and buyer stage. You get the prompt-by-prompt data showing where you appear today, where the citation gaps are, and which surfaces (tier-2 financial media, operator newsletters, Reddit, vendor comparison pages) you need to be on.

This is the open-book section. Below is the playbook we use with our fintech clients. Most of it you can start in-house tomorrow. Some of it scales only with sustained external help.

1. Audit your current AI search presence

Open ChatGPT, Perplexity, Claude, and Gemini in separate tabs. Ask each of them the five most commercial questions a buyer in your fintech segment would type, and explicitly stage-tag the prompts. The query “best AP automation” returns a different result than “best AP automation for a $10M ARR B2B SaaS.” Use the second form, because that is how buyers actually prompt.

Document who shows up, in what order, and what sources are cited. This audit takes 60 to 90 minutes and gives you the most important data point in this entire process: the gap between where you are and where the citation winners are. If you are not named at all, you have a presence problem. If you are named but ranked only in the challengers section, you have a positioning problem. If running this systematically across 30 to 50 prompts every month is more than your team has time for, this is where most companies bring in a specialist GEO agency.

2. Make your product pages AI-extractable

ChatGPT pulls content from product pages, but only from pages structured the way AI engines parse efficiently. Three fixes most fintech sites get wrong:

Schema markup for FinancialProduct and FinancialService: full Product or FinancialProduct schema with category, feeSchedule, interestRate (where applicable), offers, aggregateRating, and featureList. Most fintech sites mark up Organization only, which is not enough for category-prompt extraction.

Stage-tagged and use-case-tagged landing pages: clean /banking-for-startups, /banking-for-fintechs, /[your-tool]-vs-[competitor], and /alternatives/[incumbent] pages with structured comparison content. ChatGPT lifts comparison verdicts verbatim. Pages with explicit stage and use-case mentions get pulled into the right queries.

Transparent pricing pages: itemized fees, FX spreads, card interchange splits, and exact dollar amounts. Fintech is one of the most opaque categories in pricing. The vendors that publish clear pricing (Mercury, Rho, Ramp) get cited disproportionately. “Talk to sales” pricing pages cap your AI search visibility.

This is largely a one-time technical fix. Any competent technical SEO can do it. The compounding benefit is that the same structure improves Google rankings, which still drives a meaningful share of fintech buyer demand for the half of buyers who have not yet migrated to AI-first search.

3. Build your third-party citation network

This is the part of the playbook that takes the most patience, and it is the part most fintech marketing teams get wrong by aiming at the wrong surfaces. The instinct is to chase Wall Street Journal headlines or pitch Gartner. WSJ matters at scale. Gartner matters at enterprise. Neither is what gets you cited at the mid-market stage.

The actual surfaces that drive ChatGPT citations for $1M to $50M ARR fintechs, ranked roughly by leverage:

Get covered by tier-2 fintech publications and operator newsletters. Fintech Business Weekly, Fintech Brainfood, Not Boring (Packy McCormick), Bank Director, The Information fintech coverage. Pitch the operator writers with a clean angle (specific stage fit, real customer numbers, the trend that makes the story). One thoughtful piece in Fintech Brainfood beats ten paid placements for AI search visibility.

Publish honest vendor comparison and “alternative to” pages. “[Your tool] vs Mercury” pages that are honest about where Mercury wins. ChatGPT lifts comparison verdicts directly. Fintech buyers are paid to be skeptical; honest comparisons outperform marketing fluff by orders of magnitude.

Be a recurring presence in operator Reddit communities. r/Entrepreneur, r/fintech, r/smallbusiness, r/Banking. Not promotional posts. Real founder or operator voice answering category questions, ideally from your founder or head of growth. ChatGPT quotes Reddit when the answer reads like an operator, not a marketer.

Founder podcasts and operator newsletter features. The 20VC podcast, Fintech Brainfood podcast, Lenny’s Newsletter, First Round Review case studies. Founder-voice content carries practitioner credibility that ChatGPT weighs heavily for category queries.

Niche fintech category review sites and operator-focused blogs. waveup and similar fintech-specialist content sites publish category roundups ChatGPT cites directly. Smaller audience than a Forbes feature, dramatically higher per-mention citation weight.

There is no shortcut. The citation network is the ceiling on AI search visibility. Without sustained presence in tier-2 fintech media, on honest comparison pages, in operator Reddit threads, and in fintech-specialist content, your AI search citations cap out at the floor your own product pages provide.

4. Publish original fintech data and customer-validated proof

ChatGPT cites data. Not opinion, not thought leadership prose. Data. Annual State of [Category] reports, original customer surveys, payment volume benchmarks, churn-by-stage metrics, transaction-cost studies. If you publish a State of B2B Payments in 2026 with 400 verified responses from finance leaders and a clean methodology, you have created a citation asset AI engines will reference for the next 12 to 24 months across multiple prompt patterns.

Customer case studies count too, but only when they are specific. “ACME reduced payment processing costs” is invisible. “ACME (a 50-person B2B SaaS at $8M ARR) consolidated three payment processors into one Modern Treasury implementation and cut transaction costs 23 percent over six months with a documented migration playbook” gets quoted. Specificity, verified outcomes, stage-tagged customer context, and real customer names are the difference between case studies that drive citations and case studies that decorate your site.

5. Monitor brand-prompt presence over time

The AI search landscape changes monthly. New fintech competitors enter the cited set every quarter. Old competitors fall out as their products mature into different categories. Your visibility shifts based on what new content gets indexed, what new sources ChatGPT pulls from, and what new buyer prompts emerge in your fintech category. You need a monitoring program that re-runs the audit from step 1 every four to six weeks, tracks changes, and updates strategy quarterly based on what is shifting.

This is fundamentally a continuous program, not a project. A spreadsheet works for the first few months. After that, the volume of prompt and citation data makes it hard to spot patterns without a more structured tracking system. We documented the same dynamic in how cleantech companies get cited in AI search, where the brands that started monitoring early built moats the laggards have not closed.

Want to skip the learning curve?

We have built the fintech citation playbook across multiple client engagements, from seed-stage payment startups to Series D banking infrastructure plays. If you want to see the integrated SEO and GEO methodology in action, talk to us.

Here is the honest assessment of where mid-market fintechs typically lose ground, even after they have read the playbook above (drawn from our work with B2B brands across niches):

Capability

DIY (in-house team)

Specialist agency at scale

One-time AI search audit

Doable in 90 minutes once you know the prompts to test

Structured deliverable with prompt taxonomy by buyer segment, use case, and stage

Schema and technical fixes

Yes, with a technical SEO on staff or contractor

Standardized via fintech-specific templates

Stage-tagged comparison and pricing pages

Yes, with content and design resources

Done at scale with comparison templates and competitor-mapping data

Tier-2 fintech media placements

Slow without dedicated journalist relationships

Continuous pitching pipeline with operator-writer relationships

Reddit and operator community presence

Risky if not handled by a real founder or operator on the team

Coached with templates, then organic from credible internal founder voice

Operator newsletter and podcast features

Hard without existing fintech industry relationships

Briefing prep and relationship management across operator-newsletter networks

Original research and benchmark reports

Possible if you have a data team and fintech-specific data

Survey design, fielding, and editorial production

Brand-prompt monitoring across AI engines

Manual spreadsheet, breaks down after 3 to 6 months

Ongoing structured program with regular reporting

The DIY column is doable. We are not telling you it is not. The honest gap is sustained execution: doing all of this every month, on every prompt cluster, while also running the business. That is what specialist agencies are for.

The window is closing

Right now, most fintech companies are not actively building for AI search. The category of fintechs paying attention to GEO is small, maybe one in twelve. That means the citation surface area is uncrowded. A targeted three-month citation program can lift a mid-market fintech from “not in the table” to “in the challenger section” with surprisingly little resistance.

That window is closing fast. Fintech buyers (founders, CFOs, treasury leads) are using AI search more every quarter to shortlist vendors before the first call. Your competitors will figure this out. The brands locking in placements now are pairing GEO with paid search to capture both the AI-driven and the still-Google-driven buyers, and the cost of catching up later, when ChatGPT has crystallized its citation patterns around the brands that built early, will be three to five times higher than the cost of getting in now.

This is the same dynamic that played out with Google SEO between 2008 and 2014. The brands that invested early built moats that competitors could not dismantle a decade later. AI search is the same window, opening now.

Ready to find out where your fintech stands in AI search?

If you want to understand how your fintech currently shows up in ChatGPT, Perplexity, Claude, and Gemini, and what it would take to get into the cited set, book a free 30-minute audit. You will leave with the prompt-by-prompt data and a prioritized list of the three highest-leverage moves for your brand.

This article exists because we saw an opportunity and wrote it. It ranks because we optimized it. You found it because we know how to get found online.

That is not a coincidence. It is the entire point.

We are a search marketing agency. You are reading our content because our search marketing works. The strategies in this guide are the same ones we use to generate our own pipeline.

We are a search marketing agency specializing in integrated SEO, Google Ads, and Generative Engine Optimization (GEO) for $1M to $50M B2B brands. Fintech is one of our deepest verticals, from business banking and corporate cards to embedded payments, treasury infrastructure, lending platforms, and compliance.

Does AI search optimization work for fintech companies at any stage?

Yes. We have worked with everything from seed-stage payment startups to Series D banking infrastructure plays. Early-stage fintech benefits enormously from getting cited in alternatives and comparison prompts before the category solidifies around incumbents like Mercury, Stripe, or Brex. Later-stage fintech uses GEO to defend market share, expand into adjacent buyer segments, and capture demand that legacy SEO is missing.

How do we run the audit you mention in step 1?

Open ChatGPT, Perplexity, Claude, and Gemini and ask each the five most commercial questions a buyer in your fintech category would type, stage-tagged the way buyers actually prompt (“best business banking for a $5M ARR B2B fintech” beats “best business banking”). Document who is cited and in what order. We run this as a formal audit across 30 to 50 prompts per category as the first phase of every engagement.

How long until we see results?

For a mid-market fintech starting with weak AI search presence, expect 30 to 90 days for first measurable lift on lower-competition prompts (specific use cases, niche workflows, alternative-to queries). Six to nine months for sustained presence on the main category prompts. Twelve months to fully build the citation network across tier-2 fintech media, operator newsletters, niche review sites, and Reddit communities.

Does GEO compete with our existing SEO or PPC investment?

No. They reinforce each other. Strong product page structure, schema markup, comparison content, and authoritative backlinks all help both Google rankings and AI search citations. The work compounds rather than competes. PPC also stays valuable for high-intent commercial queries while GEO builds in the background, and fintech is one of the categories where pairing the two delivers the cleanest ROAS lift.

Can you guarantee we will be #1 in ChatGPT?

No, and no agency that is honest with you will. ChatGPT pulls from a fluid set of sources, and recommendations shift as new content gets indexed. What we can do is build the citation surface area that makes your brand structurally likely to appear in your category prompts, then monitor and adjust as the landscape changes.

What does this cost?

Engagements start at $5K per month for SEO and GEO work. Most fintech clients invest $8.5K per month across SEO, PPC, and GEO. Some venture-backed fintech brands invest over $33K per month, and they do it profitably, with returns measured in qualified pipeline, demo requests, and signed customer volume.

How is fintech GEO different from GEO for other industries?

Three differences. First, the citation sources skew heavily toward tier-2 fintech media (Fintech Business Weekly, Fintech Brainfood, The Information), operator newsletters (Not Boring, Lenny’s Newsletter, First Round Review), and Reddit communities, not the Gartner/Forrester analyst stack most marketers expect at the mid-market stage. Second, honest vendor comparison pages and “alternative to” pages carry unusually high weight because the fintech buyer is highly skeptical. Third, regulatory and compliance signals (SOC 2, PCI DSS, state licensing) materially influence which fintechs ChatGPT trusts to recommend.

Can challenger and startup fintech brands break in, or is this only for incumbents?

Yes, challengers absolutely break in. ChatGPT cites challenger fintechs in nearly every category we audited (Mercury and Rho above legacy banks, Modern Treasury and Increase above Stripe Treasury, Lithic and Highnote alongside Marqeta in card issuing, Sardine and Alloy in fraud, Puzzle and Mosaic in accounting). The “alternatives to” and “best for [stage / use case]” prompts specifically favor challengers, which is exactly where smaller fintech brands have outsized GEO leverage.

Where does ChatGPT actually pull citations from for fintech?

Not where most fintech marketing teams expect. When we ran the live queries to write this guide, ChatGPT cited tier-2 fintech publications (Wall Street Journal, Fintech Business Weekly), niche fintech review and comparison sites (waveup and similar), Reddit threads in operator subreddits (r/Entrepreneur, r/fintech), and vendor-owned comparison pages directly. Gartner and Forrester mattered less at the mid-market stage than we expected. If you are a $1M to $50M ARR fintech, the highest-leverage move is getting into tier-2 fintech media and operator newsletter coverage, plus being a real founder-voiced presence in operator subreddits.